Overspending can throw off your budget in one weekend. Then the rest of the month turns into catch-up mode. For freelancers, this feels worse because rent, renewals, and family costs do not pause.

To manage finances better this year, you need a simple reset you can repeat. This guide gives you a 7-day plan to get back on budget after overspending, rebuild a realistic budget using your last 30 days of spending, track expenses consistently with a weekly routine, cut monthly costs that drain your cash, and set up sinking funds, an emergency fund, and clear debt payoff steps.

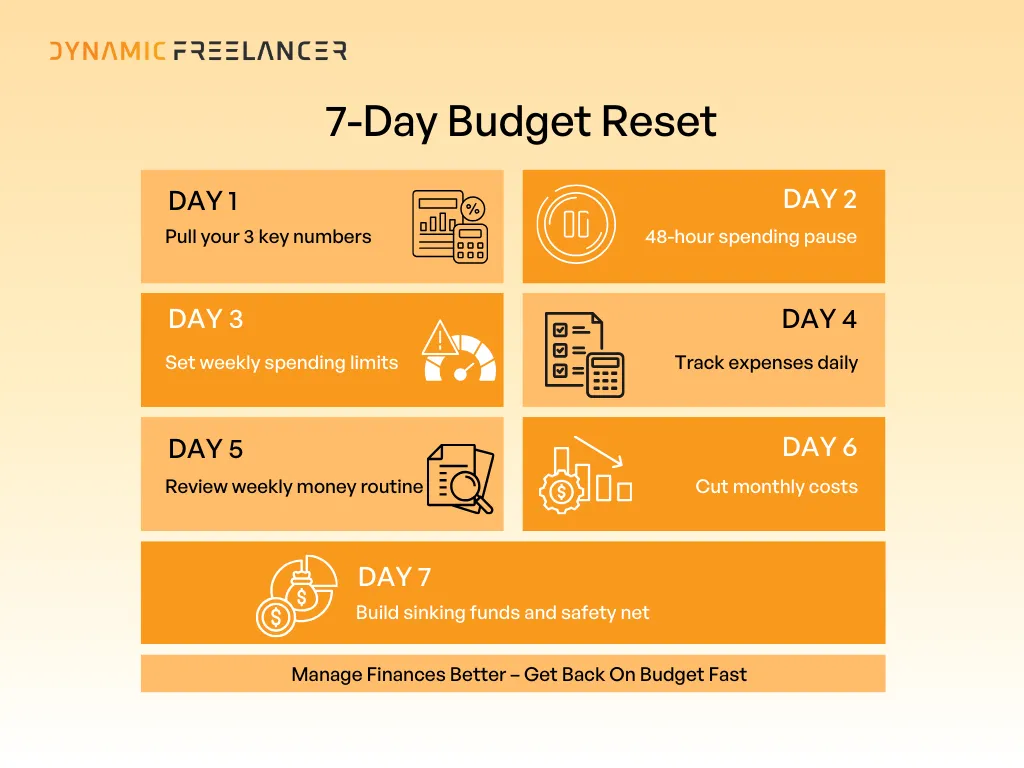

By the end, you will have a system you can run every week to stay in control all year.

Day 1: Do a Fast Budget Reset After Overspending

Pull the 3 numbers that matter

Before you change anything, get clarity. This takes 10 minutes.

Money Available Today: Your current bank balance minus any pending card charges you know are coming.

Bills Due Before Your Next Payday: Rent, phone, internet, loan payments, credit card minimums, school fees, and any fixed payments.

Your Minimum Weekly Spend: The lowest amount you need for groceries, transport, and essential work costs.

These three numbers tell you what you can protect, what you must pay, and what you can pause.

Freeze non-essential spending for 48 hours

For the next two days, stop all non-essential spending. This is the fastest way to stop the leak and create breathing room.

Pause things like:

Food delivery and dining out.

Shopping, subscriptions, and app purchases.

Taxi upgrades, impulse spends, and “small treats”.

Keep spending only on essentials you listed in your minimum weekly spend.

Cover bills and minimum payments first

Now protect your basics so you avoid late fees and stress.

Pay rent and fixed bills that are due next.

Pay minimum debt payments so you stay current.

Set aside your minimum weekly spend so you can function and work.

Once these are covered, you can plan the rest of the week with clear limits instead of guessing.

Days 2 To 3: Build a Realistic Budget from Your Last 30 Days

Turn real spending into weekly limits

Open your last 30 days of transactions and group every expense into a category. Do not rely on memory.

Use this simple approach:

List the totals per category. Groceries, transport, eating out, subscriptions, phone, rent, work tools, debt payments.

Divide each total by 4. This gives you a weekly number that matches your real life.

Set a weekly limit for the flexible categories. Food delivery, dining out, shopping, and entertainment need caps.

Weekly limits keep you on track because you correct faster. If you overspend on Monday, you still have the week to fix it.

Set a simple rule for variable income

Your budget must work in your lowest month, not your best month.

Use this rule:

Base budget: Set weekly limits that you can afford even in a low-income month.

Bonus plan: When extra money comes in, split it in this order:

Upcoming bills

Sinking funds

Emergency fund

Debt payoff

Guilt-free spending

This keeps your essentials protected.

Days 4 to 5: Track Expenses Consistently with One Simple Method

Set up a daily two-minute check-in

Pick one place to track spending. A notes app, a budgeting app, or a simple spreadsheet all work. The method does not matter as much as consistency.

Each day, do this check-in:

Record what you spent today. One line is enough.

Check your weekly limits. Look at food, transport, and lifestyle.

Make one small decision. If you are over in one category, reduce the next day’s spend to balance it.

Use a weekly money routine checklist to stay on track

Weekly checklist:

Update totals by category and compare to your weekly limits.

Pay any bills due this week and confirm the amounts.

Move money into sinking funds for upcoming costs.

Add to your emergency fund if you have surplus.

Check debt balances and confirm minimum payments are covered.

Plan the next week’s spending for food, transport, and lifestyle.

Day 6: Cut Monthly Expenses Without Breaking Your Lifestyle

Cut fixed costs first

Fixed costs move the needle fastest because they hit every month.

Start with these:

Housing: If rent is stretching you, negotiate at renewal, adjust your space, or consider a different area.

Phone and internet: Switch plans, remove add-ons, and compare offers before you renew.

Transport: If you rely on taxis, set a weekly cap and plan errands in one trip. If you drive, track fuel and parking as one category.

Insurance and fees: Review what you pay for and remove upgrades you do not use.

Pick one fixed cost to reduce this week. One change is enough to create momentum.

Remove recurring leaks and unused subscriptions

Recurring leaks are small payments that add up and drain your budget quietly.

Do a fast scan of your transactions and flag:

Subscriptions you forgot about.

Free trials that turned into charges.

Apps and tools you do not use for work.

Food delivery, coffee runs, and impulse shopping patterns.

Then set two rules:

Cancel anything you have not used in 30 days.

Keep one small “treat” budget each week, with a clear spending limit.

This keeps your lifestyle intact while your spending stays controlled.

Day 7: Set Up Sinking Funds and Your Safety Net

Pick sinking funds categories that match freelance life

Sinking funds are small savings pots for planned costs. They stop renewals and big bills from breaking your budget.

Start with 3 to 5:

Visa and renewals

Health and medical

Travel

Devices and work equipment

Car costs or family costs, if relevant

Set each one like this: target amount + due month, then divide by months left. Move the money right after you get paid.

Build an emergency fund plan with a clear starter target

Your emergency fund is for unexpected costs and slow months.

Start with:

One month of essential costs

Two months if you support dependents

Keep it in a separate account. Add to it every week, even if it is a small amount.

Follow debt payoff plan steps without falling back

Use a simple plan:

List each debt, the balance, and the minimum payment.

Pay every minimum on time.

Put extra money toward the highest interest debt.

Keep a small buffer so you do not rely on credit for basics.

Worth a look: Master Your Monthly Freelance Admin Routine

Your Money Reset Plan for the Rest of the Year

You reset after overspending, protected your bills, and set clear weekly spending limits based on your last 30 days. You tracked expenses with a quick daily check-in and a short weekly review. You also cut monthly costs, set up sinking funds for planned expenses, and built your safety net with an emergency fund and a debt payoff plan.

Keep it steady with one weekly money check. Small adjustments each week stop one expensive day from turning into a bad month.

Frequently Asked Questions

Find answers to common questions about this topic

How do I get back on budget after overspending?

How do I do a budget reset fast?

What should be in a weekly money routine checklist?

What are sinking funds, and which categories do freelancers need?

Disclaimer: This article is intended to provide practical, up-to-date information. Details may vary based on individual circumstances, location, or changes in regulations. The information provided is for informational and educational purposes only.